Is your current "tax-efficient" pay structure actually leaking thousands of pounds into HMRC's pockets? With the Personal Allowance frozen at £12,570 until 2031, many directors find themselves trapped by fiscal drag without even realising it. You've worked hard to build your business. It's only right that you keep as much of your profit as possible. Getting the right dividends vs salary advice is no longer just a once-a-year task; it's a vital strategy to ensure you aren't paying a penny more than you legally owe.

We know the stress of navigating complex thresholds and the constant fear of an unexpected tax bill. It's frustrating to feel like you're being penalised for your own success. This guide promises to help you master the most effective way to pay yourself in 2026 whilst staying fully compliant. You'll learn how to balance the £12,570 National Insurance Primary Threshold against the reduced £500 dividend allowance to achieve the highest personal net income. We'll also explore how the 15% employer National Insurance rate impacts your bottom line, giving you a clear, actionable plan for the year ahead.

Key Takeaways

- Identify the 2026 "sweet spot" by aligning your salary with the £12,570 National Insurance Primary Threshold to maintain your State Pension record without incurring tax.

- Navigate the reduced £500 dividend allowance and learn how to structure profit extractions to keep more of your hard-earned money.

- Get expert advice on dividends vs salary to understand how the narrowing gap between PAYE and dividends affects your personal net income.

- Discover why employer pension contributions are often the most tax-efficient alternative to traditional income, shielding your profits from both Corporation Tax and NICs.

- Maintain compliance and avoid HMRC penalties by using real-time bookkeeping to ensure your company has sufficient retained profits before declaring dividends.

Table of Contents

-

The Director’s Dilemma: Why Your Remuneration Strategy Matters in 2026

-

Comparing the Mechanics: How Salaries and Dividends Work Together

The Director's Dilemma: Why Your Remuneration Strategy Matters in 2026

Managing a limited company involves more than just operational success. It requires a strategic approach to extracting value from your business. This is where our core advice on **dividends vs salary **begins. Many directors assume that taking a simple salary or an arbitrary split is enough. However, without precision, you risk significant tax leakage. At Malik AccounTax Ltd, we believe avoidable liabilities shouldn't erode your hard work. We focus on protecting your bottom line from day one.

To better understand how these elements work together for your 2026 planning, watch this helpful video:

A 50/50 split is rarely the most efficient route. It ignores the subtle shifts in National Insurance and Corporation Tax rates that define the current landscape. Our "Not a penny more" promise is about finding the exact point where your personal income is maximised whilst your tax bill is minimised. This requires a tailored remuneration mix, not a generic template that fails to account for your specific profit margins.

The Role of the Director-Shareholder

You occupy a unique dual position as both an employee and a shareholder. HMRC views these income streams through different lenses. Salaries are subject to PAYE and National Insurance contributions, whereas dividends are paid from profits after Corporation Tax. Balancing these is a fine art. We help you navigate these complexities and ensure your dividend tax obligations are handled with precision.

The Impact of the 2026 Tax Landscape

The 2026 tax year brings specific challenges, particularly with frozen thresholds. The Personal Allowance is set at £12,570 and serves as the anchor for your entire strategy. As inflation impacts your business, staying static means paying more tax in real terms. Malik AccounTax Ltd acts as your proactive guardian, ensuring your pay structure evolves in line with regulations to help your business grow.

Comparing the Mechanics: How Salaries and Dividends Work Together

To master your finances, you must understand that salary and dividends are two sides of the same coin, yet HMRC treats them very differently. A director's salary is a deductible business expense. This means every pound you pay yourself as a salary reduces your company's taxable profit, effectively shielding that portion of income from Corporation Tax. However, this comes at a cost. Salaries are subject to PAYE income tax and National Insurance Contributions (NICs). With the employer NIC rate at 15% for earnings above the £5,000 secondary threshold, the "cost" of a high salary can escalate quickly.

Dividends offer a different path. These are paid from "post-tax" profits, meaning the company has already paid Corporation Tax, likely at the 19% small profits rate or the 25% main rate, before the money reaches you. Whilst dividends don't attract National Insurance, making them appear "cheaper" on the surface, they are not a deductible expense. At Malik AccounTax Ltd, we adopt a "Proactive Guardian" stance. We carefully analyse both streams to minimise your total tax exposure and protect your bottom line from unnecessary leaks. If you are unsure which mix fits your current profit levels, you can book a discovery call with our team.

The Benefits of a Small Salary

Taking a modest salary is about more than just cash flow; it's about securing your future. By staying above the Lower Earnings Limit (LEL) of £6,396 but remaining below the £12,570 Primary Threshold, you maintain your State Pension record without actually paying employee NICs. This strategy also provides the steady, predictable income history that lenders require for mortgage applications. Since most director-shareholders are exempt from the National Minimum Wage, you have the flexibility to set this figure at the most tax-efficient level for 2026.

The Power of Dividends

Dividends provide the agility every business owner needs. They allow you to reward yourself when cash flow is strong and scale back during leaner months. Even with the 2026/27 dividend allowance at a slim £500, the tax rates remain lower than standard income tax. For instance, the basic rate for dividends is 10.75%, compared to 20% for salary. When you combine this with expert dividends vs salary advice, you can navigate these thresholds with precision, ensuring you don't pay a penny more than necessary.

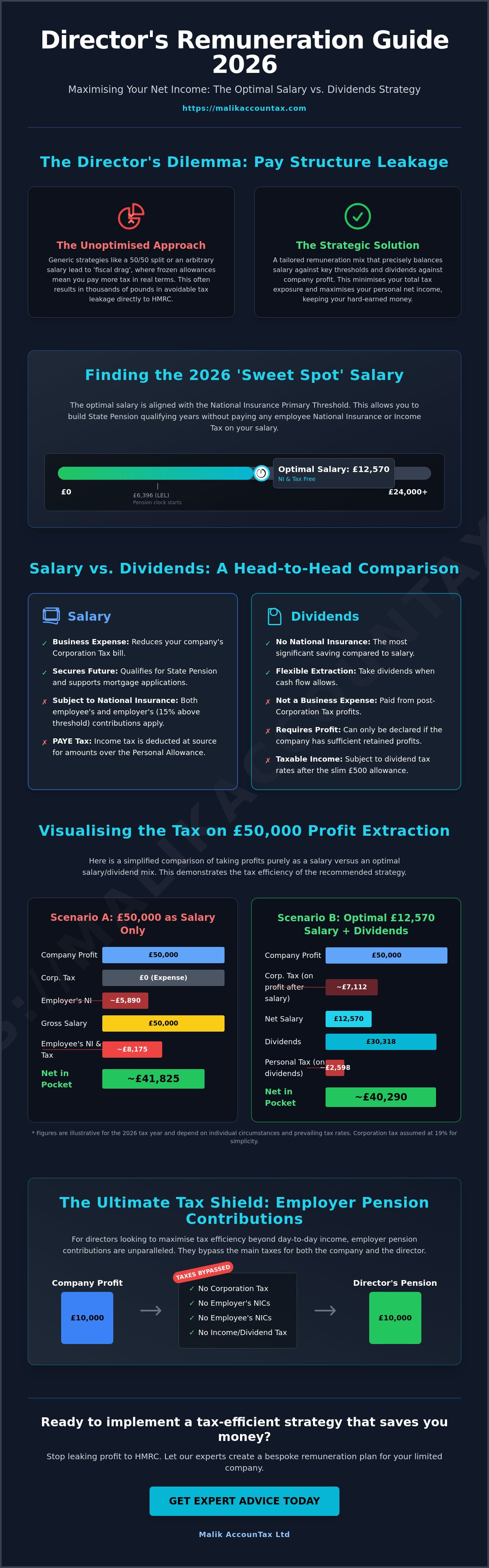

Finding the 2026 Sweet Spot: Thresholds, NICs, and Rates

Identifying the most efficient pay structure requires a surgical look at National Insurance (NI) boundaries. For the 2026/27 tax year, the Primary Threshold sits at £12,570. This is the point where you, as an employee, start paying 8% NI. However, the Secondary Threshold, where the company starts paying employer NI at 15%, is much lower at £5,000. This gap creates a strategic crossroads for every director. You must decide whether the Corporation Tax savings of a higher salary outweigh the cost of employer NI contributions.

Most dividends vs salary advice focuses on two paths. You could take a "Low Salary" aligned with the £5,000 Secondary Threshold to avoid all NI payments. Alternatively, you can opt for the "Personal Allowance Salary" of £12,570. Whilst the latter triggers roughly £1,135 in employer NI, it also acts as a larger deductible expense. If your company pays the 25% main rate of Corporation Tax, this higher salary could actually leave the business in a better net position. To explore this further, read our guide on How to Reduce Your Corporation Tax Bill. If these calculations feel overwhelming, you can request a tailored tax review to find your specific sweet spot.

Scottish Income Tax Nuances for Edinburgh Directors

For our clients in Edinburgh, the math changes. Scotland maintains its own income tax bands for non-savings and non-dividend income. With the introduction of the Advanced Rate and different thresholds for the Higher Rate, Scottish directors often hit the 45% or 48% tax marks sooner than their English counterparts. It's vital to remember that whilst your salary is taxed at Scottish rates, your dividends are taxed at the UK-wide rates. This divergence makes professional planning essential to avoid the "hidden" higher-rate traps that catch many local business owners off guard.

Maximising the Dividend Allowance

The dividend allowance for 2026 remains at a modest £500. Once you've used this tiny tax-free slice, your dividends are taxed based on your total income band. Basic rate taxpayers pay 10.75%, higher rate taxpayers pay 35.75%, and additional rate earners pay 39.35%. Unlike your salary, which is deducted at source via monthly payroll, dividend tax is not deducted at source. Instead, you'll report and pay this liability through your annual Self-Assessment tax return, making it crucial to set aside funds throughout the year to meet the January deadline.

Beyond the Numbers: Tailoring Your Income Strategy

Efficiency isn't just about the split between PAYE and profit. To truly protect your wealth, you must look at employer pension contributions. Unlike a salary, these are usually exempt from National Insurance and remain a fully deductible business expense. They provide a direct route to move money from your company to your personal future without HMRC taking a cut today. It's a "triple win" that many directors overlook when seeking advice on dividends vs salary.

Precision is your best defence. You can only legally pay dividends from retained profits. If your books aren't up to date, you're flying blind. We advocate for meticulous, real-time bookkeeping to ensure every payment is compliant and documented. This "Proactive Guardian" approach prevents the stress of HMRC penalties and ensures you're building on solid financial ground. Clear books. Confident decisions.

The Malik AccounTax Ltd Difference

Expert Services, Real Results. We don't just crunch numbers; we provide a partnership that propels your business forward. Many directors come to us because they're tired of dealing with their current accountant, who only speaks in technical jargon or remains unresponsive. At Malik AccounTax Ltd, we provide "plain English" guidance on everything from HMRC RTI compliance to complex remuneration planning. Our "Not a penny more" promise ensures your strategy is tailored specifically to the 2026-27 tax year, shielding you from avoidable tax exposure.

Next Steps for Edinburgh Startups and SMEs

It's never too late to streamline your income. Even if you're mid-way through the financial year, we can help you transition to a more efficient payment structure. Whether you're an Edinburgh-based startup or an established SME, a proactive review by Malik AccounTax Ltd can typically save you 15-30% on avoidable tax exposure. Don't let your hard-earned profits leak away through outdated advice. Book your 2026 tax efficiency review here and take control of your financial future today.

Take Control of Your 2026 Remuneration Today

Navigating the 2026 tax landscape shouldn't feel like a burden. By looking beyond simple splits and considering the pension strategies and threshold alignments we've discussed, you can secure a significantly higher personal net income. At Malik AccounTax Ltd, we pride ourselves on delivering clear, actionable expertise that cuts through the HMRC jargon. Clear books lead to confident decisions.

As Chartered Accountants in Edinburgh with deep expertise in Scottish tax nuances, we understand the specific pressures local directors face. Our clients typically save 15-30% on avoidable tax exposure by moving away from reactive, year-end accounting to our proactive model. Don't let your hard-earned profits erode due to outdated structures. Book your expert dividends vs salary advice today to ensure your business remains a tool for your growth and confidence. Let's make 2026 your most tax-efficient year yet.

Frequently Asked Questions

Is it better to take a salary or dividends in 2026?

For most limited company directors, a combination of a low salary and dividends remains the most tax-efficient strategy in 2026. Taking a salary up to the National Insurance threshold allows you to utilise your personal allowance, whilst dividends benefit from lower tax rates. This dual approach minimises your overall tax bill whilst ensuring you maintain essential social security benefits. Expert dividends vs salary advice ensures you don't pay a penny more than necessary.

How much dividend can I take tax-free in the 2026-27 tax year?

You can receive £500 in dividends tax-free during the 2026-27 tax year. This dividend allowance has been reduced significantly from the £5,000 limit seen a decade ago. Any dividend income above this £500 threshold is taxed at 10.75%, 35.75%, or 39.35%, depending on whether you're a basic, higher, or additional rate taxpayer. We help you track these thresholds in real-time to avoid unexpected Self-Assessment bills.

Do dividends count towards my State Pension?

Dividends don't count as qualifying earnings for the State Pension. To build up your 35 qualifying years for a full pension, you must receive a salary that meets the Lower Earnings Limit of £6,396 per year. This is why we always recommend a small salary alongside dividends. It protects your future retirement whilst keeping your current tax obligations as low as possible. Clear books lead to confident decisions about your future.

What is the most tax-efficient director's salary for 2026?

Aligning your salary with the National Insurance Primary Threshold of £12,570 is widely considered the most tax-efficient route for 2026. This specific figure allows you to build qualifying years for the State Pension without triggering employee National Insurance or personal income tax. Whilst the company will pay 15% employer NI on earnings over the £5,000 secondary threshold, the 19% to 25% Corporation Tax relief often makes this the most beneficial path.

Can I change my salary and dividend split halfway through the year?

You can adjust your remuneration split at any time, provided your company has sufficient retained profits to cover dividend payments. Changing a salary requires updating your payroll through HMRC RTI compliance, whilst dividends must be documented with board minutes and vouchers. Our "Proactive Guardian" approach involves reviewing your dividends vs salary advice throughout the year to ensure your strategy remains optimal as your business profits fluctuate or your personal needs change.

Disclaimer

Disclaimer: The information provided on this website is for general informational purposes only and does not constitute accounting, tax, legal, or financial advice. Whilst every effort is made to ensure accuracy, Malik AccounTax accepts no responsibility for any loss arising from reliance on the information contained on this website. Professional advice should always be obtained based on your individual circumstances.